Discover Your Path to Homeownership

Your Ultimate Guide

to Buying Property in Singapore

Navigate the Market with Confidence:

Expert Insights on HDB, Condo, and Landed Property

Explore the intricacies of buying property in Singapore with our expert guidance, tailored to help you make informed decisions every step of the way.

Download Your Free Buyer Guide Now

Which Home is right for you?

Exploring Singapore Residential Options

HDB Flats

- Affordable Public Housing:

Mass-market public housing built and managed by the Housing & Development Board (HDB).

- Government Support:

Subsidized purchase prices and CPF housing grants make them the most affordable option for Singapore citizens.

- Variety of Types:

Available in various flat types (2-room Flexi flats for singles, 3-room, 4-room, 5-room, to executive apartments and 3Gen flats) with 99-year leasehold tenure.

- Location

HDB flats are strategically located across Singapore, often in self-contained towns with amenities and services nearby.

- Community Focus:

HDB aims to create vibrant and cohesive communities with various recreational and social amenities, including playgrounds, fitness corners, neighbourhood parks and hawker centres.

Private Condominiums

- Ownership:

Private condos are privately developed non-landed residential properties, are privately owned typically either freehold or 99-year leasehold and are a common choice for those looking to upgrade from HDB flats.

- Ownership open to both citizens and foreigners (subject to Additional Buyer’s Stamp Duty for non-locals).

- Facilities:Feature gated security, landscaped grounds, and a range of facilities such as swimming pools, gyms and BBQ pits.

- Price Comparison:Higher entry price point and property taxes compared to HDB; financing subject to loan-to-value limits.

- Compared to landed properties, they are generally considered less expensive.

Landed Houses

- Ownership:

Individual homes with their own land parcels—types include terraces, semi-detached houses, and bungalows.

- Unlike condominiums or HDB flats, landed property owners have title to both the land and the house, giving them full control over the property.

- Landed property owners can renovate, rebuild, or expand their houses as they see fit, subject to URA and BCA regulations.

- Scarcity and High Demand:

Due to the limited availability of land in Singapore, landed properties are in high demand and typically more expensive than other types of housing.

- Location:

They are often located in prestigious and well-established neighborhoods.

- Purchase Restrictions:

Foreigners generally cannot purchase landed properties in Singapore, and requiring approval from the Singapore Land Authority (SLA), except in specific areas like Sentosa Cove.

Navigate the HDB Property Buyers Journey

The Journey begins by addressing the intricacies of eligibility, and the Step-by-Step Purchase Process: Understand the detailed steps for buying either new BTO/SBF or resale HDB flats, ensuring a smooth transactions.

Buying as couples/ families, seniors, or singles ?

Core family nucleus:

All core members must remain in the flat application, and physically occupy the flat during the minimum occupation period (MOP) after the flat purchase. Their names cannot be removed.

Buying a New BTO/SBF HDB Flat

All core members must remain in the flat application, and physically occupy the flat during the minimum occupation period (MOP) after the flat purchase. Their names cannot be removed.

Eligibility and Housing Grants

Step-by-Step Purchase Process

Common Pitfalls to Avoid

Buying a New HDB Flat: Eligibility Conditions

Eligible CPF Housing Grant for Buying a New HDB Flat

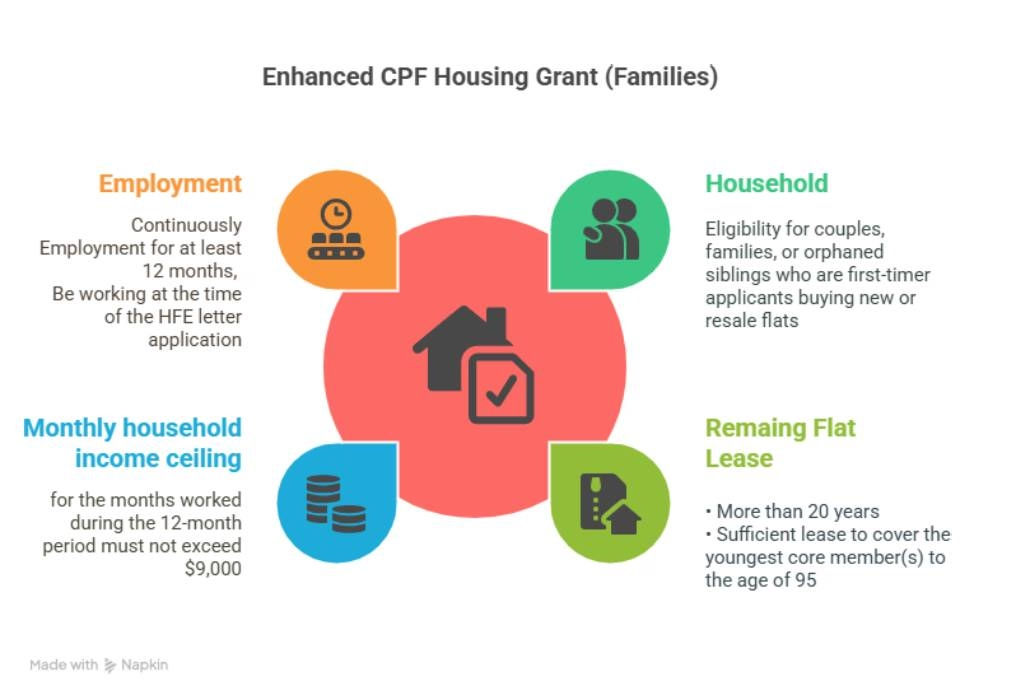

Enhanced CPF Housing Grant (Families)

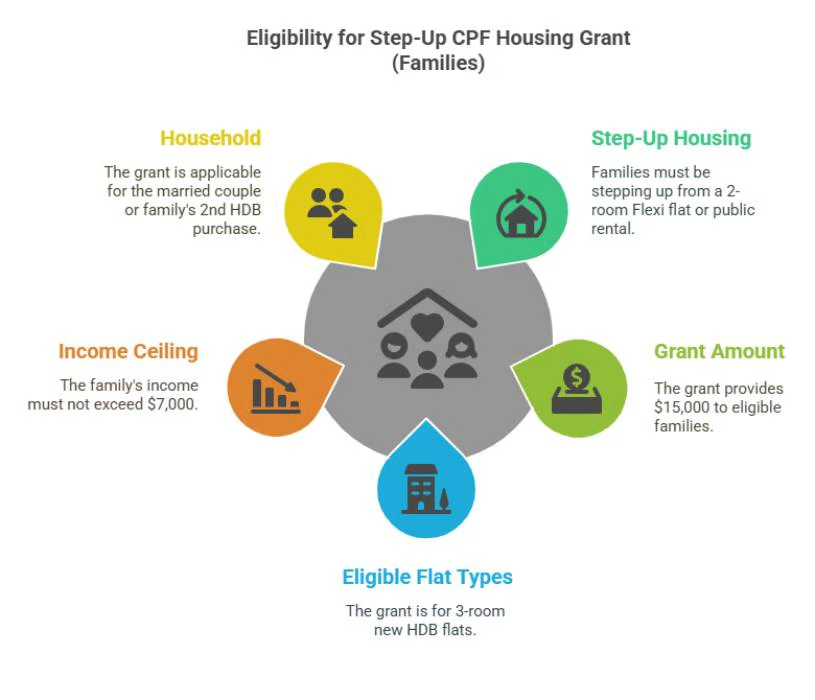

Step Up CPF Housing Grant

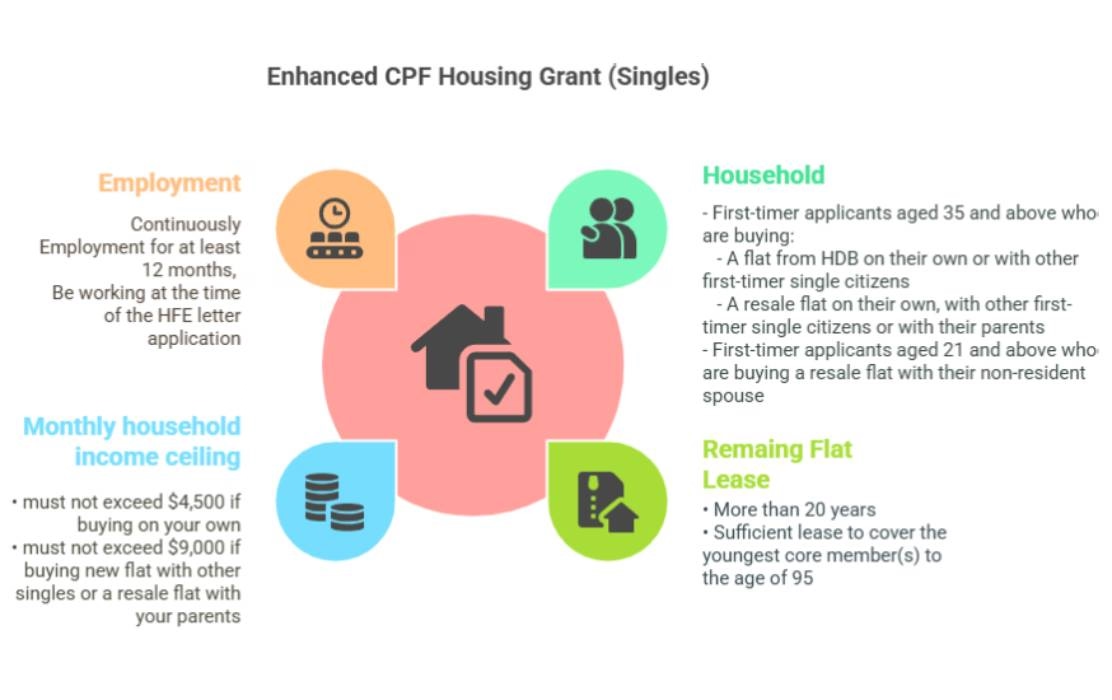

Enhanced CPF Housing Grant (Singles)

Buying a New HDB Flat

Step 1

Check Eligibility

by applying for an HDB Flat Eligibility (HFE) letter

processing time ~ 1 month

Step 2

during sales launch

receive ballot results within 2 months after the applications closed

4 weeks after the release of the ballot results

Step 3

and pay Option fee

Within 9 months after booking a flat

Step 5

Collect Keys

and pay balance purchase price

Step 4

Sign Agreement for Lease

Common Pitfalls to Avoid When Purchasing a New HDB (BTO/SBF) Flat

First-time HDB buyers often make similar mistakes due to a lack of experience in the property market

Here are some frequent pitfalls buyers fall into when purchasing a new HDB flat—and how to steer clear of them:

Insufficient Financial Planning:

- Not calculating all costs involved beyond the flat price, including stamp duties, legal fees, valuation fees, home insurance, and conservancy charges.

- Failing to set aside an emergency fund after the purchase.

- Overstretching Financial Resources (Even with Grants) – Despite housing grants, some buyers still overcommit to flat sizes or locations that strain their budget, especially when factoring in renovation costs which are often significant for new flats.

Not Understanding Housing Loans::

- Not comparing HDB loans vs. bank loans, or choosing one without fully understanding interest rates, repayment schemes, and eligibility criteria.

- Not obtaining an In-Principle Approval (IPA) from banks or an HLE letter from HDB early in the process.

Ignoring the HDB Flat Eligibility (HFE) Letter:

- As of 2023, the HFE letter is mandatory for all HDB purchases. Not obtaining it or understanding its implications for loan and grant eligibility can halt the buying process.

Missing Critical Deadlines:

- Each phase of the BTO/SBF application has specific deadlines (e.g., application submission, selection appointment, lease signing). Missing these can lead to disqualification or loss of opportunity.

Submitting Incorrect or Incomplete Documentation:

- Providing outdated income certificates, missing essential forms, or making errors in declaration can cause delays or outright rejection of the application.

Misunderstanding Eligibility Criteria:

- Applicants often misinterpret income ceilings, family nucleus requirements, or citizenship criteria, leading to an ineligible application.

- Missing out on eligible housing grants (e.g., Enhanced CPF Housing Grant, Proximity Housing Grant) due to insufficient research or misunderstanding criteria.

Focusing Solely on Price:

- Prioritizing a low price over other crucial factors like location, accessibility, flat condition, and future growth potential.

Emotional Decision-Making:

- Allowing emotions to override logical financial and practical considerations can lead to poor long-term decisions.

Not Accounting for the Long Waiting Time:

- BTO flats typically have a waiting period of several years. Buyers might not plan adequately for interim housing or unexpected delays in key collection.

- Assuming BTO flats complete “on time”—delays of 6–12 months can occur, affecting your planning and temporary housing costs.

Ignoring Unit Orientation and Layout:

- Choosing purely on price or view, without checking sun orientation (morning vs. afternoon heat). Not considering factors like afternoon sun exposure or the practical functionality of the layout can lead to discomfort or higher utility bills after moving in.

- Failing to envision furniture placement or future family needs based on the floor plan.

- Ignoring block-level factors like rubbish chute location, playground noise or road traffic at ground level.

Ignoring Future Development Plans:

- Relying heavily on unconfirmed future amenities or infrastructure projects near the BTO site for perceived value appreciation, which may or may not materialize. Assuming transport lines shown at launch will be ready by your move-in date—plans often slip.

- Not reviewing the URA Master Plan—adjacent sites may be designated for industrial, dumping, or high-rise development.

Mismanaging the Optional Component Scheme (OCS):

- Opting for OCS without carefully evaluating whether the provided finishes and fittings meet their personal preferences or quality expectations. This can lead to unnecessary hacking and additional renovation costs later.

Under-Planning Renovation:

- Budgeting only for HDB’s basic “white box” finish and neglecting electrical trunking, floor screeding or hacking costs.

- Starting renovation immediately on handover without securing renovation permit or signing with a reliable contractor—risking fines or delays.

Lack of Diligence During Defect Liability Period:

- After key collection, new flat owners have a defect liability period to report issues. A common pitfall is not thoroughly inspecting the unit for defects (e.g., cracks, faulty wiring, plumbing issues) and failing to report them to HDB promptly.

Not Factoring in Resale Levy (for Second-Timers):

- Second-time HDB flat buyers might overlook or underestimate the resale levy, which can significantly impact the overall cost of their new flat.

Disregarding the Minimum Occupation Period (MOP)::

- Underestimating the commitment of the 5-year MOP, during which the flat cannot be sold or rented out entirely. This can hinder future upgrade plans.

By drilling down on these tailored questions and steering clear of these common missteps, you’ll set yourself up for a smoother BTO or SBF journey from application through to move-in.

Buying a Resale HDB Flat

Eligibility and Housing Grants

Step-by-Step Purchase Process

Key Questions and Common Mistakes

Buying a Resale HDB Flat: Eligibility Conditions

Eligible CPF Housing Grant for Buying a Resale HDB Flat

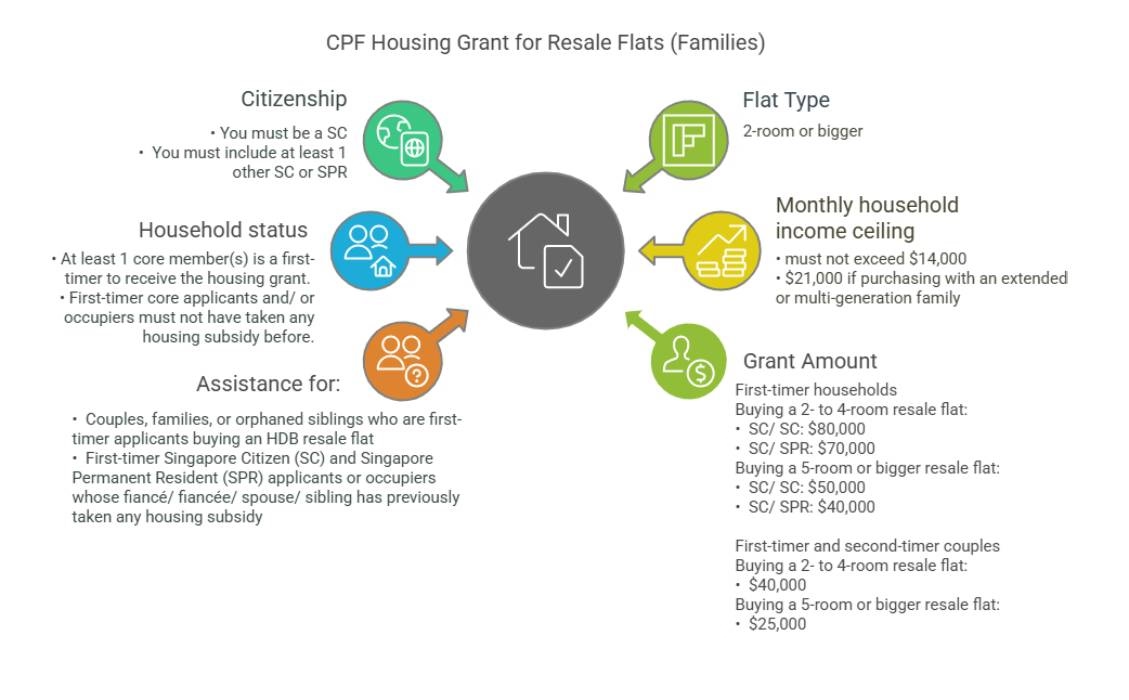

CPF Housing Grants for Resale Flats (Families)

Enhanced CPF Housing Grant (Families)

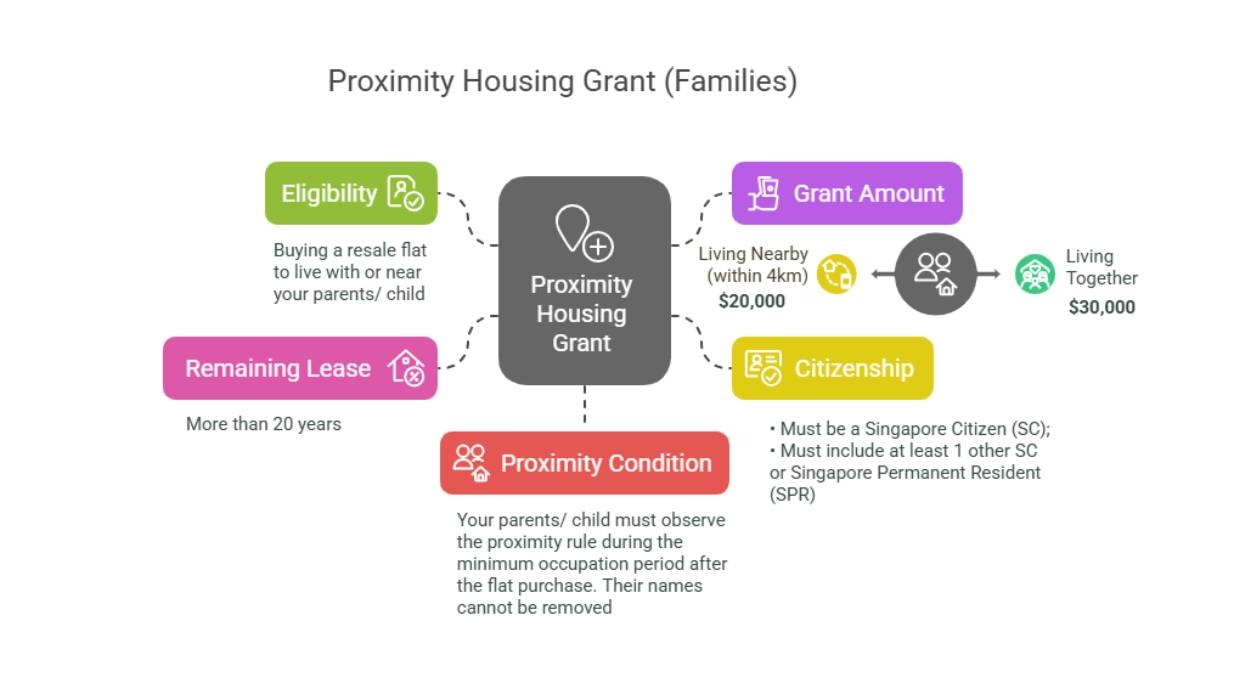

Proximity Housing Grant (Families)

Step Up CPF Housing Grant

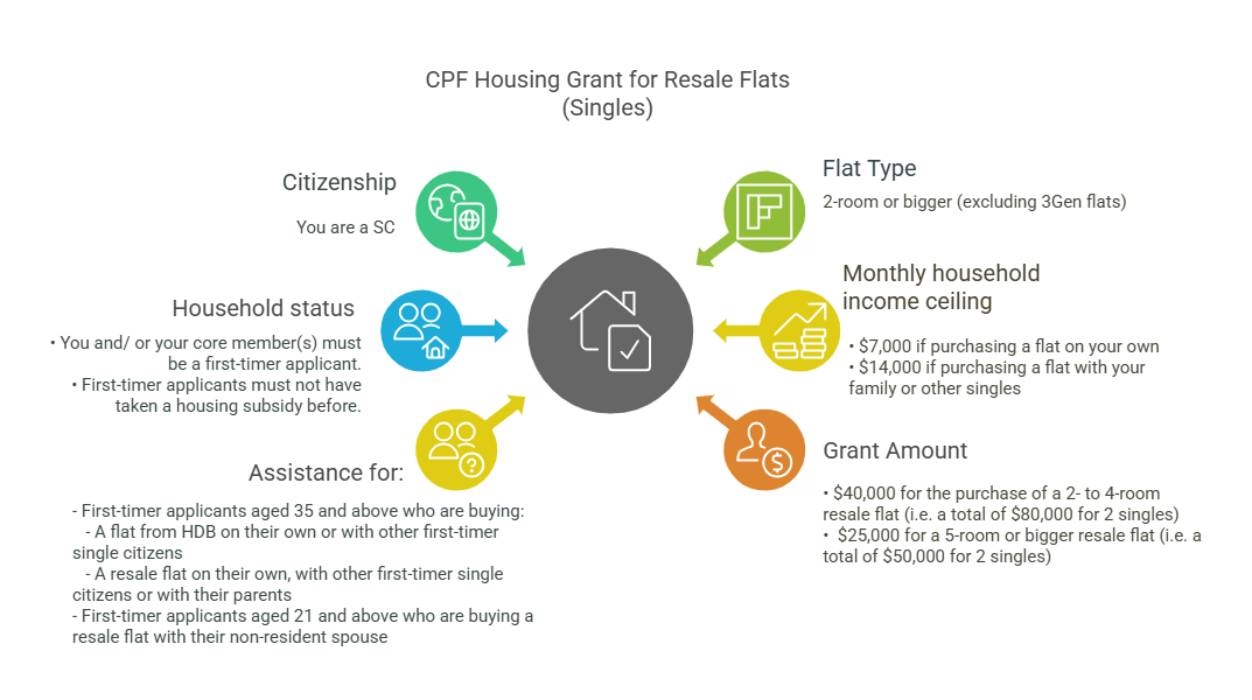

CPF Housing Grant for Resale Flats (Singles)

Enhanced CPF Housing Grant (Singles)

Proximity Housing Grant (Singles)

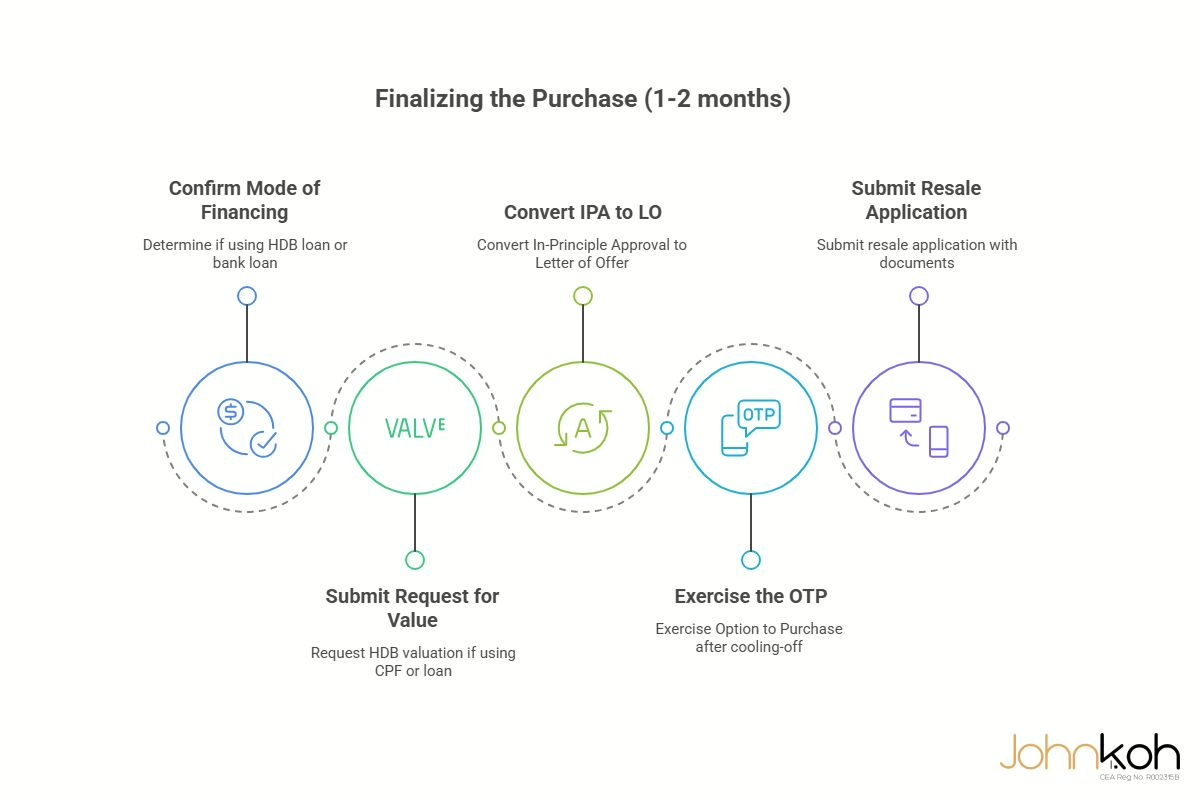

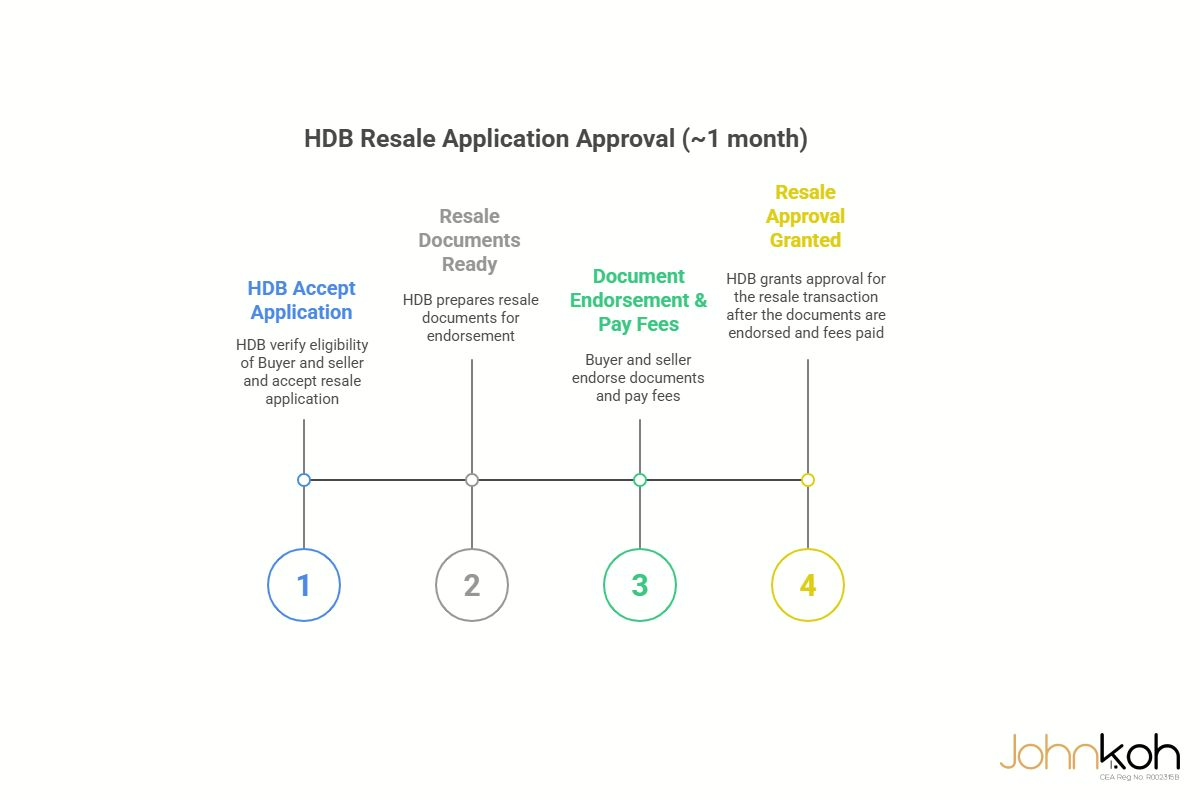

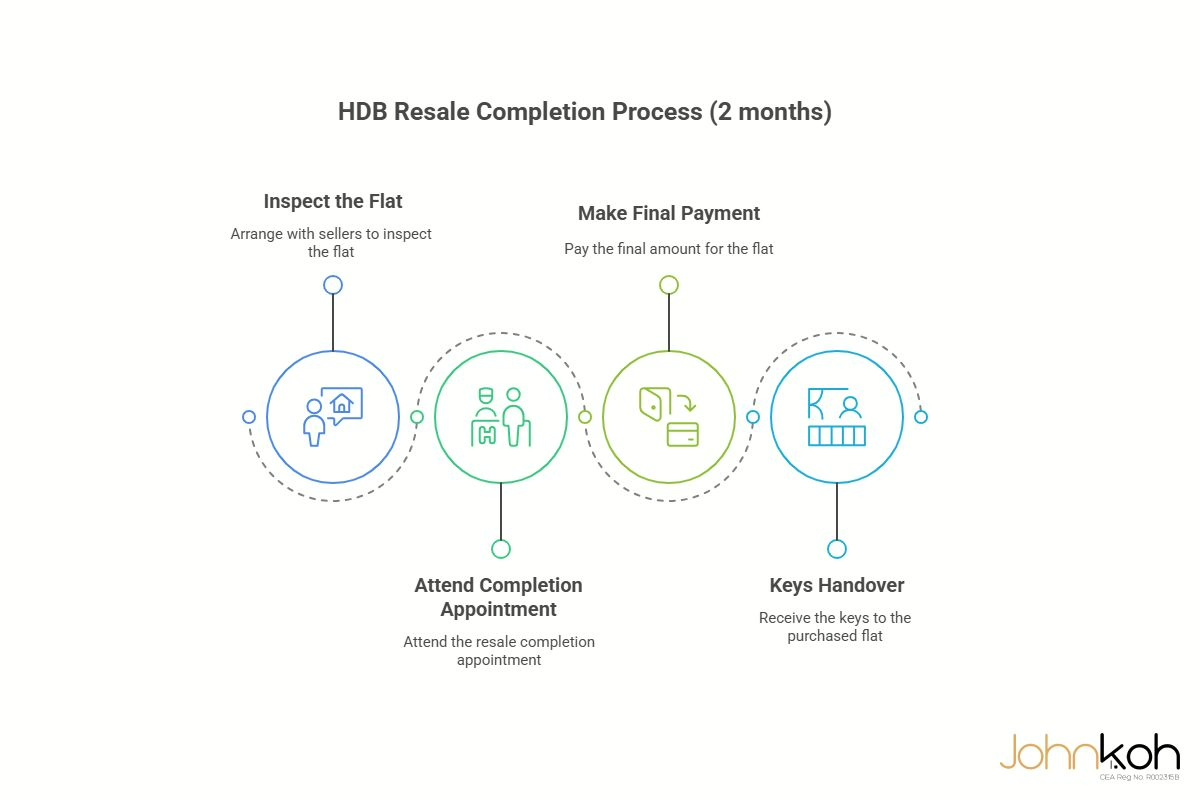

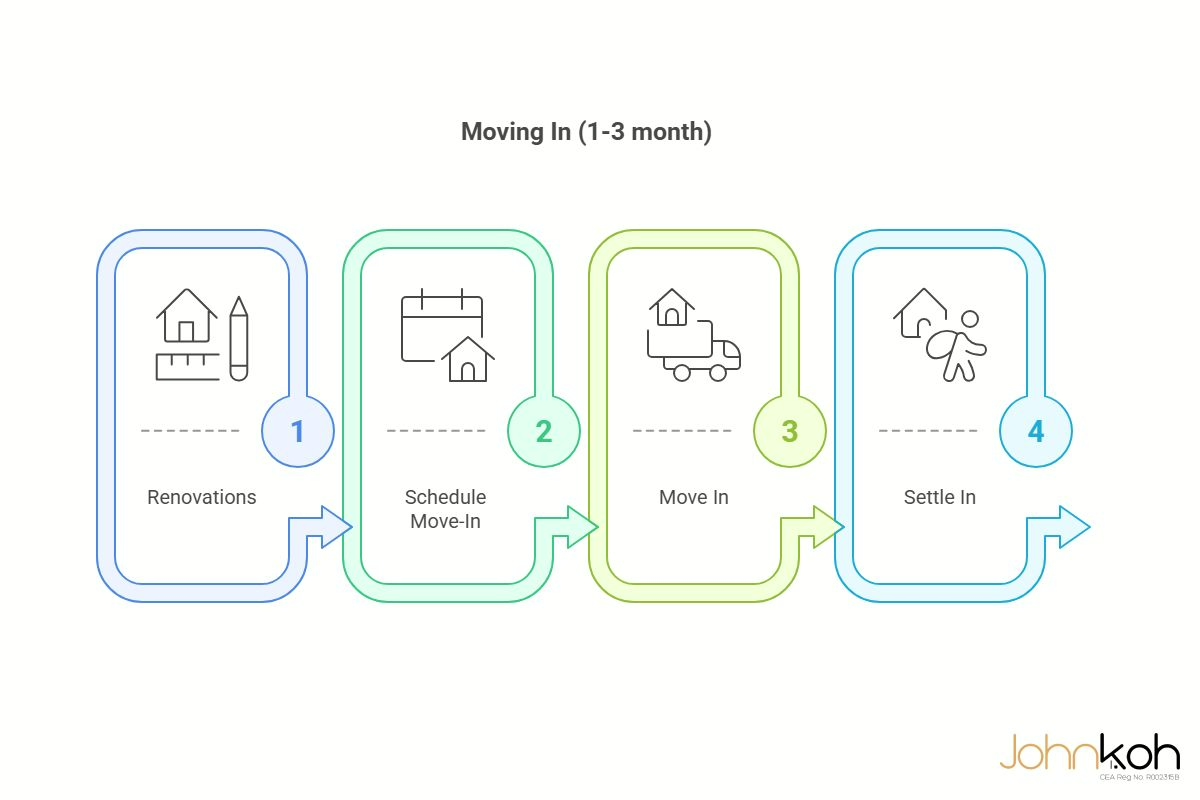

Buying a Resale HDB Flat

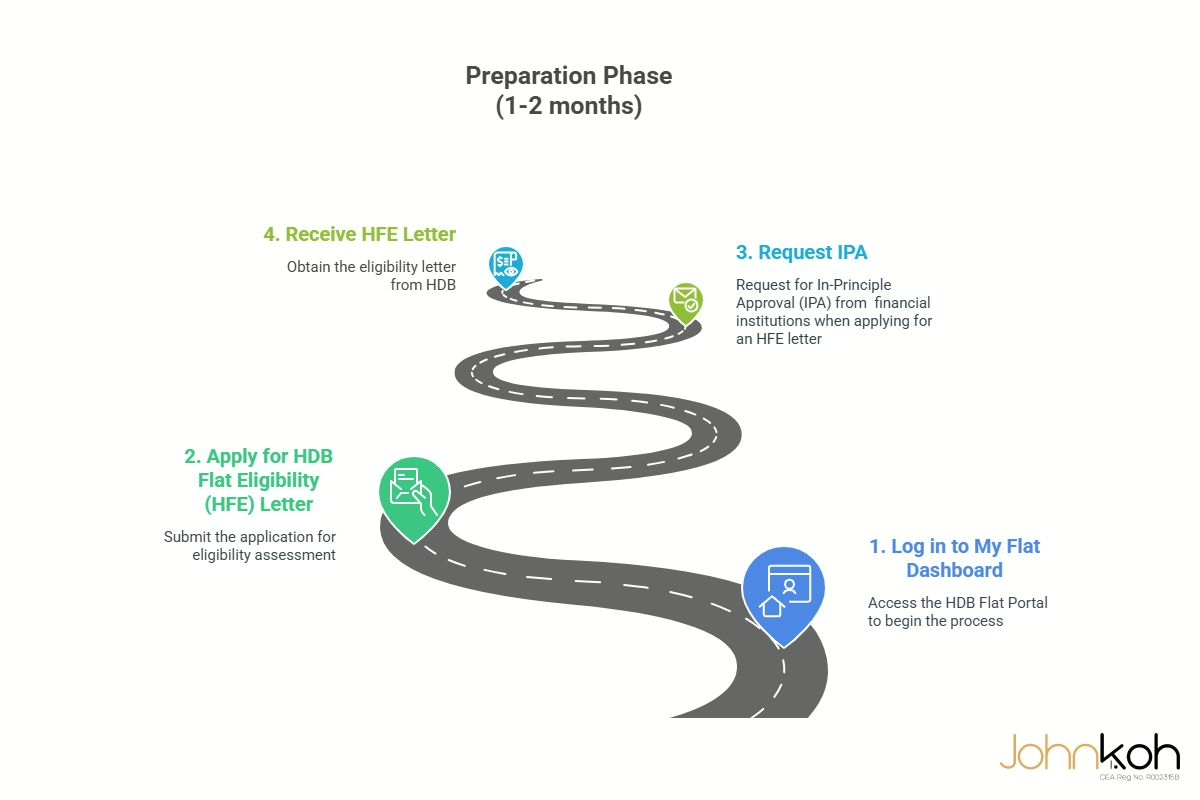

1. Preparation Phase

2. Searching for a Flat

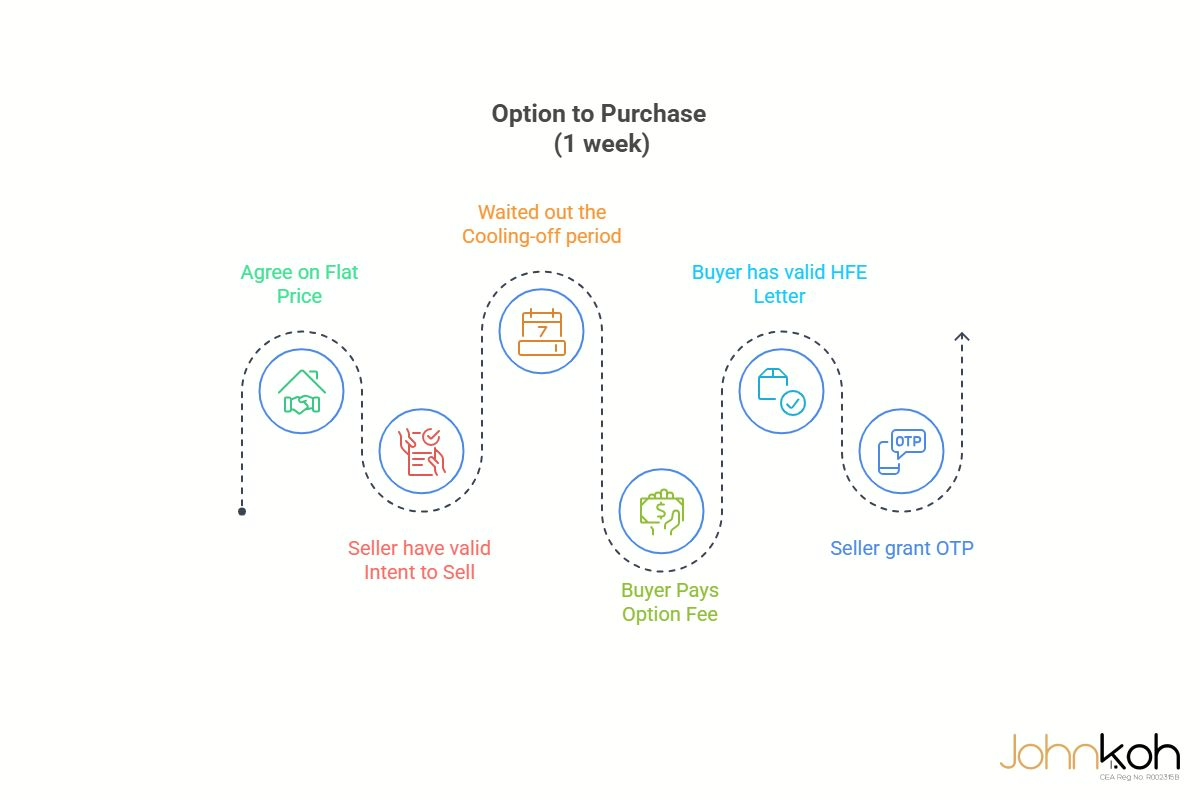

3. Obtain the OTP

4. Finalize the Purchase

5. HDB Resale Application Approval

6. Completion Of Sale

7. Move In

Key Questions to Ask When Buying a Resale HDB Flat

Here are some key questions you might ask yourself (or your agent/seller) under each critical area when considering an HDB purchase:

Location and Accessibility:

-

Does the site front onto major roads (noise) or face a park (view)?

-

How far is the nearest MRT station and bus stop? Is there a sheltered walk?

-

How long does it typically take to walk to the nearest amenities like supermarkets, hawker centres, or clinics?

-

Are there dedicated bicycle lanes or pedestrian-friendly routes around the block?

-

What is the typical peak-hour commute time to key destinations?

-

Are there any major road works or future transportation plans in the area? (Check URA Master Plan)

-

Which primary schools are within a 1km radius?

Liveability and Condition:

-

What is the size and layout of the flat? Can I see the floor plan?

-

Is the unit facing the sun in the morning or afternoon? Does it get very hot?

-

Is there adequate natural light and ventilation in the unit?

-

Can others easily look into the flat from the corridor or opposite units?

-

How old is the flat and when was the last renovation or major repair?

-

What is the remaining lease on the flat?

-

Are there any visible signs of wear—wall cracks, water seepage, rust?

-

What is the condition of the flooring, walls, and ceilings? Are there any cracks, mould, or water leakage?

Neighbourhood:

-

What are the neighbours like? Have there been any issues with noise or disputes?

-

Have there been any problems with illegal moneylenders in the block or estate?

-

Do noise sources or late-night activities (e.g. kopitiam, function rooms) impact quiet hours?

-

Is there a precinct pavilion nearby and how often is it used? (Can it get noisy?)

-

Where are the refuse collection points located? Are they near the unit?

Unit Specifics:

-

Has the owner done any renovations? If so, were they approved by HDB?

-

Are there any existing fixtures that will be included in the sale? What is their condition?

-

Have there been any pest infestations in the unit or block?

-

Is there a bomb shelter in the unit and is the door original?

Seller's Situation:

- Why is the seller moving—urgent sale, upgrading, relocating overseas?

- Do the sellers require an extension of stay after the sale? If so, for how long?

-

What is the seller’s timeline for completing the sale?

Financials:

- What is the asking price versus recent transacted prices for similar flats?

- How much CPF can you apply, and what are your cash-out–of–pocket estimates?

-

Are there any outstanding maintenance fees or conservancy charges?

Use these to guide your due diligence, compare properties, and negotiate with confidence.

Common Mistakes to Avoid When Purchasing a Resale HDB Flat

Here are some frequent pitfalls buyers fall into when purchasing an HDB flat—and how to steer clear of them:

Mismanaging Financing:

- Not calculating all costs involved beyond the flat price, including stamp duties, legal fees, agent commissions, valuation fees, home insurance, and conservancy charges.

- Over-leveraging CPF balance and leaving too little in your Ordinary Account for retirement.

- Misunderstanding how much CPF can be used for the downpayment and monthly installments, especially for older flats with shorter leases.

- Skipping pre-approval: Not obtaining an In-Principle Approval (IPA) from a bank or an HDB Loan Eligibility (HLE) letter before committing to a purchase — only to find out later your loan quantum or interest package isn’t as expected.

- Not comparing HDB loans vs. bank loans, or choosing one without fully understanding interest rates, repayment schemes, and eligibility criteria.

- Failing to set aside an emergency fund after the purchase.

Underestimating Renovation Costs:

- Many older resale flats require extensive renovations to modernize or repair existing structures. Buyers often underestimate these costs, leading to financial strain.

- Failure to budget for hacking, rewiring, plumbing overhauls, and interior design can quickly deplete savings.

Lack of Research on Grants and Schemes:

- Missing out on eligible housing grants (e.g., Enhanced CPF Housing Grant, Proximity Housing Grant) due to insufficient research or misunderstanding criteria.

Ignoring the HDB Flat Eligibility (HFE) Letter:

- As of 2023, the HFE letter is mandatory for all HDB purchases. Not obtaining it or understanding its implications for loan and grant eligibility can halt the buying process.

HDB Flat Eligibility (HFE) Letter Delays:

- While more crucial for new flats, even resale buyers now need an HFE letter. Delay in obtaining this can hold up the purchase process.

Emotional Buying:

- Falling in love with a flat’s aesthetics without properly assessing its practicalities (e.g., inconvenient location, poor layout, noise levels) can lead to buyer’s remorse.

- Not verifying estate planning—adjacent land parcels could be redeveloped into undesirable uses.

Neglecting Future Needs:

- Overlooking lease decay impact on resale or loan eligibility 20–30 years down the road – For older resale flats, the remaining lease affects the property’s potential and value for future appreciation. It can also impact CPF usage and loan eligibility, especially for leases below 60 years.

- Purchasing a flat that might be too small for a growing family or too large if children eventually move out,

- Not considering accessibility features if elderly family members might reside there in the future.

- Failing to consider proximity to schools, eldercare or future MRT lines that may open years later.

Skipping Detailed Inspection:

- Focusing solely on aesthetics and missing hidden structural issues (leaks, cracks, spalling).

- Without a thorough inspection, buyers might miss underlying structural problems, leaky pipes, or electrical issues that could lead to costly repairs after purchase.

- Not engaging a qualified inspector for older flats is a common oversight.

Overlooking the Minimum Occupation Period (MOP) of the Previous Owner:

- Buyers might mistakenly assume they can move in immediately, not realizing the seller’s MOP has not been fulfilled. This can lead to delays in key collection.

Overlooking the implication of the Minimum Occupation Period (MOP):

- Underestimating the commitment of the 5-year MOP, during which the flat cannot be sold or rented out entirely. This can hinder future upgrade plans.

By consciously avoiding these missteps—factoring in both upfront and ongoing costs, giving yourself time to compare options, planning for the long term, securing financing prudently, carrying out comprehensive inspections, and analyzing location trade-offs—you’ll be in a much stronger position to make a confident, informed purchase.

The Private Condominium Buyer's Journey

Guiding potential buyers through the process of purchasing a private condominium in Singapore, highlighting the eligibility requirements and the steps involved.

Eligibility Criteria

Begin your journey by understanding the eligibility criteria for purchasing a private condominium in Singapore. With fewer restrictions, these properties are accessible to Singaporeans, PRs, and Foreigners.

Step-by-Step Purchase Process

Key Questions and Concerns When Buying a Condo

Who Can Buy

Singapore Citizens (SCs):

• No quota or approval restrictions.

• Pay Buyer’s Stamp Duty (BSD) plus Additional Buyer’s Stamp Duty (ABSD) only on second and subsequent properties (20% for 2nd, 30% for 3rd-and-beyond)

Singapore Permanent Residents (PRs):

• Free to purchase, but must pay ABSD of 5% on their first property, 30% on their second, and 35% thereafter.

Foreigners:

• No need for special approval to buy an apartment/condominium. (although there might be restrictions on buying units in buildings under six storey)

• Subject to a flat 60% ABSD on top of BSD.

• 10-year restriction on Executive Condominiums (ECs) purchases for foreigners – can only do so after the property has reached its 10-year mark and has been fully privatized.

Entities (Companies, Trusts, etc.):

• Can acquire condo units but incur ABSD of 65%.

Foreign-Ownership Exceptions & Remissions:

- Nationals and Permanent Residents of Iceland, Liechtenstein, Norway or Switzerland

- Nationals of the United States of America

Age and Legal Capacity

- You must be at least 21 years old to take up a housing loan or sign a sale agreement independently.

- Minors may purchase only via a court-sanctioned arrangement (e.g., trust).

Financing and Loan Limits

- First Housing Loan (no existing residential debt): up to 75 % of the lower of purchase price or valuation.

- Second Housing Loan: up to 45 % (or 25 % if loan tenure > 30 years or repayment would extend you past age 65).

- Third & Subsequent Loans: up to 35 % (or 15 % if tenure > 30 years or extends past age 65).

- Minimum Cash Down-Payment: at least 5 % of property price must be cash if borrowing at 75 % LTV; higher cash components apply at lower LTVs.

Total Debt Servicing Ratio (TDSR):

- Your total monthly debt repayments (including the new condo loan) must not exceed 55% of your gross monthly income.

Stress-Test Rate:

- Banks must ensure you can service your loan even if rates rise to 4% (the mandated floor rate for assessments).

Stamp Duties

- Buyer’s Stamp Duty (BSD): tiered on property value (1% on the first S$180 000; 2% on the next S$180 000; 3% on the next S$640 000; 4% on the remainder).

- Additional Buyer’s Stamp Duty (ABSD): varies by residency and number of properties as outlined above.

Step-by-Step Purchase Process for New Launch Condos:

Step 1

Financial Planning & Pre-Approval

Assess your budget and secure an In-Principle Approval (IPA) from your bank

Step 2

Register Interest (Optional)

Sign up for preview invitations to gain priority access at launch

Step 3

Shortlist & Visit Showflat

Compare developments, visit show-flats, and pick your preferred unit

Step 6

Sign Sales & Purchase Agreement (S&P)

You have a timeframe (usually 3 weeks) to exercise the OTP by signing the S&P.

Within 3-weeks from Sales and Purchase Agreement (S&P) Delivery

Step 5

Loan Approval & Legal Representation

Finalize loan and obtain the formal Letter of Offer (LO) from your bank.Engage a conveyancing lawyer to review the S&P agreement and represent your interests.

The developer will deliver the S&P within 2 weeks of issuing the OTP.

Step 4

Booking & Option to Purchase (OTP)

Pay Booking fee (5% Cash) to secure your preferred unit.

The developer will issue an OTP, which gives you a period to decide whether to proceed with the purchase.

Step 7

Pay Duties & Complete

Pay the Buyer’s Stamp Duty (BSD) and potentially the Additional Buyer’s Stamp Duty (ABSD) within two weeks of signing the S&P.

Step 8

Settle Balance Down Payment

Within eight weeks from signing OTP, to pay the remaining 15% down payment (Cash and/or CPF) .

Step 9

Progressive Payments

During construction, your bank shall disburse progressive payments based on the project’s milestones, as outlined in the S&P.

Step 10

TOP & Keys Collection

Collect keys upon obtaining Temporary Occupation Permit (TOP).

Step-by-Step Purchase Process for Resale Condos:

Step 1

Financial Planning & IPA

Assess your budget and secure an In-Principle Approval (IPA) from your bank

Step 2

Engage an Agent (Recommended)

Appoint a licensed real-estate agent to help source listings and negotiate on your behalf

Step 3

Search & View

Browse property portals, shortlist suitable units and arrange viewings

Step 6

Finalize Loan & Receive Letter of Offer (LO)

Submit your full loan application and secure the bank’s Letter Of Offer (LO).

Typically 14 days, during which you can conduct due diligence (e.g., engaging a conveyancing lawyer, obtaining bank LO, etc).

Step 5

Obtain the Option to Purchase (OTP)

Pay a 1% Option fee to the seller and receive the OTP

Step 4

Negotiate & Make an Offer

Agree on a price with the seller and submit your offer

Step 7

Exercise the OTP

Pay the 4% Exercise fee (Cashier Order) to Seller’s lawyer law firm’s Conveyancing Account.

Step 8

Pay Stamp Duties

Settle Buyer’s Stamp Duty (BSD), Additional BSD (if applicable) and the balance purchase price.

Step 9

Completion & Keys Collection

Collect the keys and officially take ownership.

Key Questions & Concerns When Buying a Condo

Potential condominium buyers should consider several key questions and be aware of potential concerns before making a purchase.

Freehold vs. Leasehold:

-

Understanding whether the property is freehold (indefinite ownership) or leasehold (typically 99 years) is crucial due to its implications for the property’s value and future resale.

Condition of the unit (for resale):

-

For resale condos, it is essential to thoroughly check the unit for any existing defects or signs of wear and tear.

Condo Management & Rules:

-

Inquire about the Management Corporation Strata Title (MCST), including the amount of maintenance fees, the health of the sinking fund, and any rules or restrictions imposed by the management. For older developments, it’s also worth considering the potential for an en-bloc sale.

Unit Layout and Size:

-

Ensure that the layout and size of the unit meet your specific needs and consider the efficiency of the layout to maximize usable space.

Facing and View:

-

Consider the direction the unit faces in relation to the sun, as this can affect the temperature and natural light within the unit. Also, inquire about any potential future developments that might obstruct the view.

Noise and Privacy:

-

Evaluate the potential noise levels from surrounding areas or within the development itself, and consider the level of privacy the unit offers.

Amenities and Facilities:

-

Assess the quality and usability of the shared amenities and facilities, such as the swimming pool and gym, and understand the costs associated with their maintenance.

Resale Value and Investment Potential:

-

Research the historical price trends in the area and consider the location’s desirability and potential for future appreciation. If you plan to rent out the property, also consider its rental income potential.

The Landed Property Buyer's Journey

Eligibility & Regulations for Landed Property Ownership

Learn about the eligibility and regulations for owning landed property in Singapore.

Step-by-Step Purchase Process

The process of buying landed property in Singapore shares similarities with condominium purchases but often involves a greater emphasis on due diligence and financial planning.

Important Factors and Questions to Consider

Consider important factors like property type, location, and financing options. Make well-informed choices with our comprehensive guidance.

Eligibilty Criteria for Landed Property Ownership

WHO CAN BUY?

Owning landed property in land-scarce Singapore is highly coveted, and as such, it comes with the strictest eligibility criteria. Primarily, landed property ownership is restricted to Singapore Citizens.

Foreigners (i.e. non-Singapore Citizens, including Singapore Permanent Residents) are required to obtain approval from the Singapore Land Authority (SLA) Land Dealings Approval Unit (LDAU) under the Residential Property Act (RPA) to purchase landed residential.

WHAT ARE THE CRITERIA FOR APPROVAL?

Each applicant is assessed on a case-by-case basis, taking into consideration, including but not limited to, the following factors:

- You should be a permanent resident of Singapore for at least five years; and

- You must make exceptional economic contribution to Singapore. This is assessed taking into consideration factors such as your employment income assessable for tax in Singapore.

Types of landed properties that require SLA approval for PRs and Foreigners include:

Landed properties are classified as restricted properties for foreign ownership. This is because foreign ownership of landed residential properties in Singapore is restricted under the RPA to ensure that such properties remain the primary preserve of Singapore Citizens.

- Vacant residential land;

- Terrace house;

- Semi-detached house;

- Bungalow (detached house);

- Strata landed house, which is not within an approved condominium development under the Planning Act (e.g., townhouse or cluster house). In other words, such houses may be part of a shared community with common facilities but are not granted condominium status;

- Shophouse (for non-commercial use);

- Landed residential property at Sentosa Cove.

Some applications may take longer to process and this can typically range from 2 – 6 months.

Applying for an in-principle approval first

Foreigners/PRs should look out for relevant clauses in the Option to Purchase (OTP) if you need time to get approval from the LDAU. This is because once the OTP is exercised, you can be liable for forfeiture of monies paid ( typically 1+4%) if the LDAU approval is not granted.

Since the processing time requires 1 to 6 months, it is not realistic to get the LDAU approval before exercising the OTP since the Option period is 2 weeks.

It is therefore recommended to apply for an in-principle approval first before looking for a property or entering into any contract to purchase a restricted property.

Step-by-Step Purchase Process for Landed houses:

Step 1

Engage a real estate agent (highly recommended)

A landed-specialized agent who the expertise to navigate this segment of the market

Step 2

Financial planning, securing financing & obtain necessary approvals (for PRs/Foreigners)

Obtain bank IPA; and SLA in-principal approvals (for foreigners/PRs)

Step 3

House hunt & Viewings

identify the specific property of interest; performing title searches to verify ownership and check for any restrictions or encumbrances on the land

Step 6

Finalize Loan & Receive Letter of Offer (LO)

Submit your full loan application and secure the bank’s Letter Of Offer (LO).

Step 5

Obtain the Option to Purchase (OTP)

Pay a 1% Option fee to the seller and receive the OTP

Step 4

Negotiate & Make an Offer

Agree on a price with the seller and submit your offer

Step 7

Exercise the OTP

Pay the 4% Exercise fee (Cashier Order) to Seller’s lawyer law firm’s Conveyancing Account.

Step 8

Pay Stamp Duties

Settle Buyer’s Stamp Duty (BSD), Additional BSD (if applicable) and the balance purchase price.

Step 9

Completion & Keys Collection

Collect the keys and officially take ownership.

Important Factors and Questions to Consider When Buying a Landed Property

When considering the purchase of landed property in Singapore, several important factors and questions should be taken into account.

Property Type and Tenure:

-

Understand the different types of landed properties available, such as terrace houses, semi-detached houses, bungalows, Good Class Bungalows (GCBs), and cluster houses. Also, determine whether the property is freehold (indefinite ownership) or leasehold (typically 99-year or 999-year tenure).

Location and Accessibility:

-

Consider the property’s proximity to essential amenities, transportation links, and any future development plans in the area as outlined in the URA Master Plan.

Property Condition:

-

Conduct a thorough inspection of the property to identify any structural issues, leakages, fractures, or signs of pest infestations, particularly termites. For older properties, factor in potential maintenance costs.

Land Titles and Caveats:

-

Verify the ownership of the land and check for any caveats or restrictions, or encumbrances that might affect its use or future development.

Zoning and Building Regulations:

-

Be aware of the zoning laws and any building height limits or conservation guidelines that might apply to the property. If you have plans for redevelopment, understand the allowable building levels and any restrictions.

Orientation and Natural Lighting:

-

Consider the orientation of the house to maximize natural sunlight and ventilation, which can impact comfort and energy efficiency.

Soil Quality:

-

If you are considering any future extensions or redevelopment, the quality of the soil can be an important factor.

Provision for future amenities:

-

Check if the property allows lift installation or other features you may want to add.

Neighbourhood:

-

Assess the surrounding environment, including noise levels, traffic conditions, and the overall community vibe.

Potential for Capital Appreciation:

-

Research past transaction trends and market conditions to gauge the property’s potential for future price appreciation.

Financing Your Property Purchase in Singapore

Securing the right financing is a critical step in the property buying journey. Singapore offers various loan options depending on the type of property you intend to purchase.

Financing Options Overview

Loan Type

HDB Loan

Bank Loan

Eligibility

Loan-to-Value (LTV)

Down Payment (Cash)

Interest Rates

Pegged to CPF OA rate (2.5%) + 0.1%

Early Repayment Penalty

Penalty charged for early repayment within the lock-in period

Late Payment

Max Loan Tenure

35 years for non-HDB properties.

Refinancing to Other

Property Type Applicability

Understanding Key Financial Metrics

Mortgage servicing ratio (MSR)

Mortgage servicing ratio (MSR) refers to the portion of a borrower’s gross monthly income that goes towards repaying all property loans, including the loan being applied for.

MSR is capped at 30% of a borrower’s gross monthly income.

It applies only to housing loans for the purchase of an HDB flat, or an executive condominium where the minimum occupation period of the executive condominium has not expired.

Total Debt Servicing Ratio (TDSR)

Total debt servicing ratio (TDSR) refers to the portion of a borrower’s gross monthly income that goes towards repaying the monthly debt obligations, including the loan being applied for.

A borrower’s TDSR should be less than or equal to 55%.

Income-Weighted Average Age (IWAA)

Income Weighted Average Age (IWAA) was introduced by MAS for the calculation of loan tenure.

Only affects joint applicants of a property and it serves to provide a better gauge of their combined ability to repay the loan

Loan Tenure

The maximum loan tenure for housing loans is capped at:

- 30 years for HDB flats.

- 35 years for non-HDB properties.

LTV Limits and Minimum Downpayment for Individuals

Apply the lower LTV limit if the loan tenure exceeds 30 years (or 25 years for HDB flats), or the loan period extends beyond the borrower’s age of 65 years.

LTV Limits for Shell Companies

If the borrower is a shell company or not an individual, the LTV limit is 15%.

Importance of Financial Planning

Thorough financial planning is essential before embarking on your property purchase journey. This includes carefully assessing your affordability and creating a detailed budget that accounts for all potential costs, such as the down payment, stamp duty, legal and agent fees, potential renovations, and the ongoing monthly mortgage repayments. It is also prudent to consider long-term financial commitments and factor in the possibility of interest rate fluctuations, especially if you opt for a floating-rate bank loan. The availability of both HDB and bank loans offers different financial pathways, depending on the property type and the buyer’s specific eligibility. Government regulations like TDSR and MSR play a crucial role in promoting responsible borrowing and ensuring that buyers do not overextend themselves financially.

Essential Considerations for Every Singapore Property Buyer

Regardless of the type of property you are considering, there are several essential factors that every buyer in Singapore should keep in mind for a smoother and more successful purchase.

Working with a Real Estate Agent

- Engage an agent with deep local market knowledge and strong negotiation skills

- Leverage their insights on neighbourhoods, price trends and potential pitfalls

- Let them handle complex paperwork, and advise which version of Conditions Of Sale to use

- Note: for private-property deals, commission is co-broking between seller’s and buyer’s agents—buyers need NOT pay

As a real estate expert in Singapore, I can offer personalized assistance, guiding you through every step of the process and ensuring you make informed decisions.

Understanding Stamp Duties and Legal Fees

- Buyer’s Stamp Duty (BSD)

Buyer’s Stamp Duty (BSD) is applicable to all property purchases, whether it’s an HDB flat, a condominium, or a landed property, and it is calculated on a tiered basis based on the property’s purchase price or market value, whichever is higher.

Buyer’s Stamp Duty (BSD) Rates (as of Current Date: May 2025)

| Property Value Range | BSD Rate | Quick BSD calculation |

|---|---|---|

| First $180,000 | 1% | 1% x purchase price |

| Next $180,000 | 2% | 2% x purchase price |

| Next $640,000 | 3% | (3% x purchase price) – $5,400 |

| Next $500,000 | 4% | (4% x purchase price) – $15,400 |

| Next $1.5 million | 5% | (4% x purchase price) – $30,400 |

| In excess of $3 million | 6% | (6% x purchase price) – $60,400 |

- Additional Buyer’s Stamp Duty (ABSD)

- Conveyancing (Legal) Fees

The ABSD rates vary for Singapore Citizens, Permanent Residents, and Foreigners, with higher rates generally applying to non-citizens and those purchasing subsequent properties.

Covers title searches, document preparation and lawyer’s professional charges.

The Importance of Location and Amenities

- Transport Connectivity

- Essential Amenities

The location of a property is a fundamental factor that significantly influences its value, liveability, and potential for appreciation in Singapore.

Proximity to MRT stations, bus stops and major arterial roads, is highly desirable as it offers convenience and accessibility.

Access to essential amenities such as reputable schools, well-stocked supermarkets, comprehensive healthcare facilities, and various recreational option plays a crucial role in enhancing the quality of life and the property’s attractiveness to potential buyers or tenants.

- Future Development

Check URA Master Plan for upcoming infrastructure, commercial or residential projects.

Planning for the Future

- Lifestyle & Family Needs

- Career & Mobility

Room for family growth, home office setups or multigenerational living.

Ease of commute to current workplace and flexibility for future job moves.

- Investment & Resale Potential

Capital-appreciation prospects, lease-decay considerations and target buyer demographics.

Ready to Find Your Dream Property? Take the Next Step

Your Journey to Homeownership Starts Here

To move forward with your property search, I am here to offer personalized assistance tailored to your specific needs and preferences.

I encourage you to contact me today for a free, no-obligation consultation. We can discuss your property requirements, explore your financing options, and navigate the Singapore real estate market together. You can reach me through the contact form below, or feel free to call me directly or send an email via the contact details as follow.

Message Me

Fill out the form below to get started on your journey to owning a home in Singapore. Our team is ready to guide you every step of the way.

Ready to Find Your Dream Property? Take the Next Step

Your Journey to Homeownership Starts Here

To move forward with your property search, I am here to offer personalized assistance tailored to your specific needs and preferences.

I encourage you to contact me today for a free, no-obligation consultation. We can discuss your property requirements, explore your financing options, and navigate the Singapore real estate market together. You can reach me through the contact form below, or feel free to call me directly or send an email via the contact details as follow.

Message Me

Fill out the form below to get started on your journey to owning a home in Singapore. Our team is ready to guide you every step of the way.

Take the Next Step

Conclusion

Our comprehensive guide is designed to equip you with the knowledge and tools needed to navigate the Singapore property market confidently. Whether you’re buying your first home or investing in real estate, our resources and expert advice will help you make informed decisions. Don’t hesitate to reach out for personalized assistance and take the next step towards securing your ideal property. I am committed to assisting you in finding your ideal home and making your property ownership dreams a reality. Take the next step today and let’s begin this exciting journey together.